Business Not As Usual

In an earlier post a description was given of a new ecologically-oriented economic system being built in response to the climate and ecological emergencies. The new economy is described as being constructed largely through two decades of transformation (the 2020’s and 2030’s).

The climate emergency and the ecological emergency are intertwined, with impacts occuring much on the same short timescales. By way of example, we all depend upon the oceans for our survival, but the oceans are dying as a consequence of aquatic environmental pollution from toxic chemicals, such as herbicides, pesticides, oxybenzone, PCBs, PBDE, PFOS, DBT, and plastic. According to a paper by the Goes Foundation:

“we have lost 40% to 50% of all life in the oceans over the last 70 years and will, over the next 25 years, continue to see a drop in ocean productivity by up to 1% year on year … by 2045 we will have lost 75% to 80% of all marine life … the oceanic tipping point is a pH of 7.95 which we reach by 2045/50 under RCP 8.5 from the IPCC … ecosystems will start crashing … we may lose the planktonic plants that are the life support system and climate regulator for our planet”

The crash of ocean ecosystems would have severe negative impacts on earth’s climate systems given the critical role that oceans play in absorbing carbon dioxide. With life on earth in-the-balance, the race is on to safeguard and preserve life-support systems.

Every aspect of human endeavour is likely to be affected as life-support systems are pushed further to collapse. Specifically in relation to the climate emergency, the Australian Security Leaders Climate Group notes

“Climate change represents an unprecedented existential security threat, undermining the stability of our planetary systems, with both current and oncoming implications across the full spectrum of human endeavour – from families and communities, to the nation-state and regional and international bilateral relations.”

The recent (April 2021) Leaders Summit on Climate provides a strong indication of crucial changes in policy that are emerging amongst governments, bringing about a clear emphasis on raising ambition and stimulating innovation. The changes include shifts in ‘enforcement direction‘. The disclosure of active involvement of intelligence services in monitoring pollution activities and climate commitments is an early indication of the powerful changes that are happening. If Earth’s life-support systems are crashed, much of the framework and foundation of which traditional concepts, such as national security, are based become largely meaningless.

The intertwined climate and ecological emergencies provide us with very clear timescales over which action will need to have been delivered. The projected crash of ocean ecosystems, projected to occur around mid-century, puts a hard-stop (three decades) on the timeline for humans to have largely completed the transformation work that needs to be done. Thus, the two decades – the 2020’s and 2030’s – are effectively now the only ones left to have made the essential changes.

The Great Leap Sideways

It is clear to many that Business As Usual (BAU) has run its course and the imperative for enterprises, from nation states to the smallest of enterprises, during the Great Leap Sideways is to navigate the new course. The process begins abruptly in the early 2020’s as economies pivot in search of the new way forward. Figure 1 shows the economy splintering, with elements attempting to remain with BAU and others, recognising that BAU is not viable, leaping sideways onto a new historic passage.

Over the two decades spanning the 2020’s and 2030’s, unprecedented changes are expected to occur. Already, for example, we are seeing new markets, such as plant-based markets, emerging rapidly in response to people turning away from meat and dairy for ethical, health and environmental reasons. The rate at which these new markets have developed, as illustrated by enterprise maps, indicates what can be achieved when there is a will to act. According to one report “By 2030, demand for cow products will have fallen by 70%. Before we reach this point, the U.S. cattle industry will be effectively bankrupt. By 2035, demand for cow products will have shrunk by 80% to 90%. Other livestock markets such as chicken, pig, and fish will follow a similar trajectory.”

Figure 1. The Great Leap Sideways (off the BAU pathway).

Some sectors, however, are continuing their dogged progression on the BAU pathway. According to one study (of four of the Oil majors) this is a reflection of what CEOs are being incentivised to achieve with the authors of the study concluding that “it is unlikely that the executives and directors at these four companies will decide to proactively decarbonise in line with climate science”. A report Banking on Climate Chaos 2021 analysing fossil fuel financing from the world’s 60 largest commercial and investment banks — aggregating their leading roles in lending and underwriting of debt and equity issuances — finds that these banks poured a total of $3.8 trillion into fossil fuels from 2016–2020. The overall fossil fuel financing trend of the last five years is still heading in the wrong direction.

A variety of approaches show that across different systems there is a spread across the pivot point indicated in Figure 1. Examples include:

- InfluenceMap‘s 2021 analysis of the largest asset owners shows that shows most asset managers are still moving too slowly when it comes to using their clout to drive change in investee companies. The portfolios managed by the top global firms continue to be misaligned with Paris climate goals in key climate-risk sectors of automotive, oil/gas/coal production, and electric power.

- Climate Action Tracker provides an analysis of countries, regions, sectors, indicators and scenarios in relation to pledges to act on climate change. Overall, the message is that “huge gaps remain”.

Proceeding with the Pivot

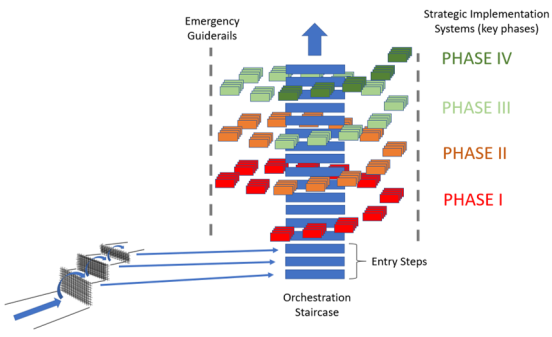

We are clearly at a stage in the bifurcation (Figure 1) during which systems are straddling across the two pathways. That situation cannot last; it is highly unstable. Initial stages in the overall development are through an orchestration staircase. Early forms of orchestration include various disclosure systems and scoring systems to inform benchmarking and league tables, some of which have been around for the best part of two decades. More sophisticated approaches, particularly in the financial and insurance sectors, have emerged more recently.

Initial steps on the orchestration staircase are generally informed by Emergency Guiderails, such as science-based targets for greenhouse gas emissions. There are many aspects to these guiderails although a key feature reflects the necessity to both reduce pollution of the natural world (as noted above in relation to ocean acidification) and remove pollution which has accumulated.

Figure 2. Initial steps on the orchestration staircase.

The spirals shown in Figure 2 represent elements which are used to drive organisations through the transformation and discontinuous change. These include building platforms for change, building decision point capabilities, management training, problem solving, monitoring and controlling processes, launching implementation projects, building competencies and capacity, and developing supportive cultures and power structures. Much of this activity is about deccelerating and halting the catastrophic impact of the mode of industrial growth, which has been decoupled from ecology.

The new economy that is being formed will, by the end of the 2020’s, be amazingly different to the type we are used to. Within the new system, structures are built up in succession through an evolutionary progression of phases. Each phase is characterised by distinct functionalities, characteristics and phenomena. Roughly, the first ten phases represent the building of the foundation of the new ecologically-oriented economy, and the phases thereafter constitute the superstructure. Very little that exists in the old economy is expected to survive intact through this overall progression, shown in Figure 3.

The timeline for the development shown in Figure 3 is 2020-2040 (as illustrated in an earlier post on navigation). Within the progression shown in Figure 3 there is a complex, dynamic system organising itself in response to severe constraints (such as the need to bend the ocean pH curve upwards and away from catastrophic acidification at pH 7.95 and runaway climate change which would be induced).

Figure 3. Evolutionary progression of the new economy.

Strandings and the Race for Relevance

As the new economy develops, the potential for businesses to become stranded on the BAU pathway increases. A stage is expected to occur when development of the new economy accelerates and the old economy begins to disintegrate at speed. This stage (during Phase V, described below, and occurring in the mid-to-late 2020’s) is likely to witness significant asset and silo stranding as well as attempts to jump off the BAU pathway into the new economy. This process is illustrated in Figure 4. Some of the jumping is likely to be government-assisted, although increasingly the problem of security of life-support systems is likely to be prioritised over protection of legacy industrial systems.

Figure 4. Stranded assets, silo jumping and deep impact.

According to the recent energy report by RethinkX

“We are on the cusp of the fastest, deepest, most profound disruption of the energy sector in over a century. Like most disruptions, this one is being driven by the convergence of several key technologies whose costs and capabilities have been improving on consistent and predictable trajectories – namely, solar photovoltaic power, wind power, and lithium-ion battery energy storage. Our analysis shows that 100% clean electricity from the combination of solar, wind, and batteries (SWB) is both physically possible and economically affordable across the entire continental United States as well as the overwhelming majority of other populated regions of the world by 2030. Adoption of SWB is growing exponentially worldwide and disruption is now inevitable because by 2030 they will offer the cheapest electricity option for most regions. Coal, gas, and nuclear power assets will become stranded during the 2020s, and no new investment in these technologies is rational from this point forward.”

Studies by Mecure and co-workers suggests that a sharp slump in the value of fossil fuels is likely before 2035 based on current patterns of energy use. Examining the impacts of new low and zero emissions technology on multiple countries, their modelling suggests countries that continue to base their economies on fossil fuel exploration, use, and export will suffer the most economic harm. The studies, although insightful in terms of the way they address the energy transition, are not subject to super-constraints, such as disintegration of life-support systems. Recognition of such super-constraints brings about a much-needed resolution of shorter timescales over which ecological reality needs to be reflected in economic affairs.

Change gathers momentum

In the early stages of development of the new economy, there are likely to be unprecedented levels of innovation. Many of these are technological although much of the innovation (technological innovations included) involve change in the ways that human endeavours relate and respond to the natural world. The innovations occur across all phases but begin to support an increasingly aligned response to the climate and ecological emergencies. The first few phases in the evolution of the new economy are:

- Conditioning (Phase I) – Conditioning of enterprises to engage, embark and continue their journeys into the new ecologically-oriented economy.

- Coordination (Phase II) – Increasing coordination across enterprises to facilitate greater cooperative responses, particularly across supply chains and within and across sectors and communities.

- Transformation (Phase III) – Initial transformation of some enterprise systems with a view to competitive and cooperative positioning in an emergent superstructure.

- Eversion (Phase IV) – Turning inside-out and upside-down of many conventional enterprise and governance systems and structures as well as value systems. This phase is characterised by strong movements, some of which are extensive shedding across the economy, waves of enterprise assimilation, and progressive engagement of governments in the forming and building of new sectors. World markets are likely to be fluctuating wildly during the eversion phase as enterprises race to find relevance.

- Supershock (Phase V) – A phase of reckoning for the old economic systems and breakthrough and consolidation of new ones. Slumps, crashes, asset stranding and asset stripping occurs at scale during this phase. Reverberations occur across the embryonic (new form) economy as some assets from distressed sectors (Figure 4) on the BAU pathway are inserted and/or ejected. This phase represents a complex, dynamic nonlinear system organising itself in response to severe constraints imposed largely from the natural world.

- Constriction (Phase VI) – A phase of crisis response as deterioration of life-support systems accelerates. This phase includes also Natech constrictions (interaction between natural disasters and industrial accidents), some of which leak into other phases. A key feature of this phase is the emergence of Directed Capitalism, governed and moved by the state in pursuance of preservation of life support systems (directional periods analogous to this have occurred during times of war). An example of such direction is government-mandated provision of insur-resilience services, through which (re)insurance companies are given licence to operate provided that insurance cover drives fast transformation of insureds.

- Pivot (Phase VII) – A phase of resets, reorientations and reconstructions occurring at multiple scales.

These and later phases, including through the superstructure (Figure 3), will be described in detail in later posts. The superstructure is a highly complex system that brings about much-needed symbiosis with the natural world.

Intensification of action

Within Phases I, II and III enterprises will be adopting numerous programmes of increasingly faster change, both in terms of scale and scope. Although many of these programmes will involve processes and activities practised on relatively restricted scales and scopes in previous years (see examples here), the timescales and logical (hard) constraints imposed by potential life-support systems collapse, induces a new cadence, intensification and fierceness of action. Examples include:

- Resource Productivity and Ecodesign – eg: elimination and substitution (eg of toxic chemicals and materials in products); reuse and remanufacturing; operational reduction, streamlining and optimisation; design of goods and services for reduced climate and ecological impact.

- New Business Models – eg: building transparency and visualisation (eg through the supply chain); value chain productivity (including digital value chains); customer coalitions and collaborative journeys; design of non-polluting organisations; environmental and resource monitoring/assessment.

- Inspired by and working with Nature – eg: circular enterprise; green chemistry; biomaterials, natural capital accounting, approaches allowing regeneration of Nature.

- Enterprise Awareness and Intelligence – eg: monitoring earth and climate systems; monitoring oceanic systems; digital twins (proximal, remote, hybrid); traceability and benefit tracking (eg through enterprise networks); building competitive and cooperative intelligence (and strategy).

- Clean-Up – eg programmes for removal of pollution from the ocean.

- Trust – eg: trustworthy disclosure of pollution streams; forensic identification of deceptive practices, pollution streams and other actions impacting climate/ecological systems.

- Protocols – eg: bans on production of toxic items and closing pollution loops through strong regulation; laws to incentivise behaviour change; laws to administer and enforce Rights of Nature.

Quest for dependability

Life-support systems are clearly critical. If we take an approach familiar to the design of engineering systems, various attributes of criticality can be identified: Reliability, Availability, Safety, and Security. These attributes of criticality lie at the heart of dependability, an essential feature of a critical system.

In effect a key priority through the 2020’s, 2030’s and beyond is to address the dependability of life support systems. Given such pressing timescales, the Earth Computer, indicated in Figure 3 as part of the emerging new economy, is likely to be a critical enabler for the accelerated transformation.

The Earth Computer, would by no means be a simple technology, and like the internet, would not be a single computer but rather a system. It is an operating, computational and stewardship system to guide and assist with criticality, including reliability, availability, maintainability, safety and security of the earth life support systems, such as the dependable (safe) climate system and dependable ecosystems. The Earth Computer would inherently be a distributed system through which multiple enterprise and governance systems work. For example, one of the key indicators for dependability of life-support systems is ocean pH (with pH 7.95 representing a critical value).

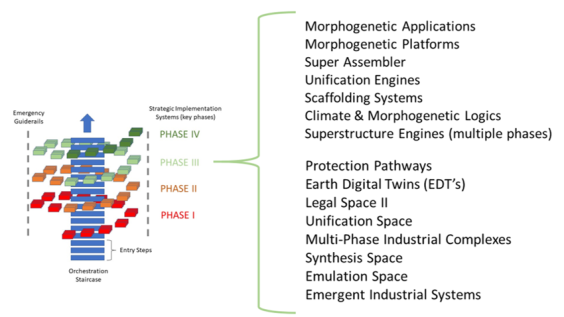

Figure 5 illustrates some of the innovations that have been identified in Phase III. Many of these innovations play crucial roles in the early development of the Earth Computer. Some of these interactions, particularly in the formative phases of the superstructure (Figure 3) lead to remarkable transformations of the Earth Computer, and these in turn influence power structures (and power struggles) at a planetary scale.

Figure 5. Examples of innovations in Phase III.

Strategic responsiveness

Approaches are already available for accelerating the transformation of enterprises on the orchestration staircase. Some of these acceleration processes rely on the concept of ‘Digital Twin’, which is a sophisticated digital counterpart of the physical system. Digital twins can use both information fed directly from within a facility (eg oil refinery, production facility, building) or information from outside the facility (such as that obtained by satellite or drone). Remote Digital Twins, for example, rely on images and other remote sensing by means of drones, satellites, and other systems that work at-a-distance together with simulations/models specific of the remote plant or facility (eg refinery). Some RDTs include sophisticated analytics that can estimate the energy, water and material used by a facility as well as estimate the waste, pollution and emissions. The analytics can quickly identify, quantify and prioritise hundreds of resource and cost saving measures for a facility – opening the way to orchestrated transformation of global supply chains. A range of satellite observatory systems using sophisticated at-a-distance monitoring and mapping systems (e.g. for methane) is emerging. The powerful impact of digital twins comes about as physical, remote and hybrid digital twins are deployed at scale to address the climate and ecological emergencies. This gives rise to the development of Earth Digital Twins (indicated in Figure 5), Ocean Digital Twins, National Digital Twins, City Digital Twins, Supply Chain Digital Twins, Investment Portfolio Digital Twins and many others. As these Digital Twins emerge and begin to inform and influence policies, decision making, legal systems and action-taking about the destabilisation and collapse of life-support systems, rates of change will ramp up. This is what leads to Eversion (Phase 4) and Supershock (Phase 5) and prepares the ground for the unprecedent developments through the 2030’s.

The changes described here are not restricted to one specific sector because everything will be in state of flux. Naturally the phases and the dynamics of enterprises existing and evolving through them are not separate; they mutually exist, one giving rise to the other, and co-evolving in a self-consistent manner. The phases also are highly interconnected. Responding to the changes outlined here is not just about building more wind turbines, installing more solar panels, or developing electric vehicles while reducing coal and other fossil fuel consumptions. Yes, those activities are involved. Enterprises will need to embark on wholesale review of why and how they exist, how they might evolve through the changes, when and where those changes might occur and the likely impacts they will bring. Given the potential for sharp degradation of life-support systems over short timescales, heightened levels of situational awareness will be required. This in turn means that enterprises will need to develop heightened skills and capabilities in strategic responsiveness, with a primary relationship being the one with Nature. That will require new forms of leadership, very different from that prevalent during the post-climax of the old economy.

You must be logged in to post a comment.